ITC Under GST Explained: Eligibility, Ineligible Credits and ITC Reversal

30-Second Summary

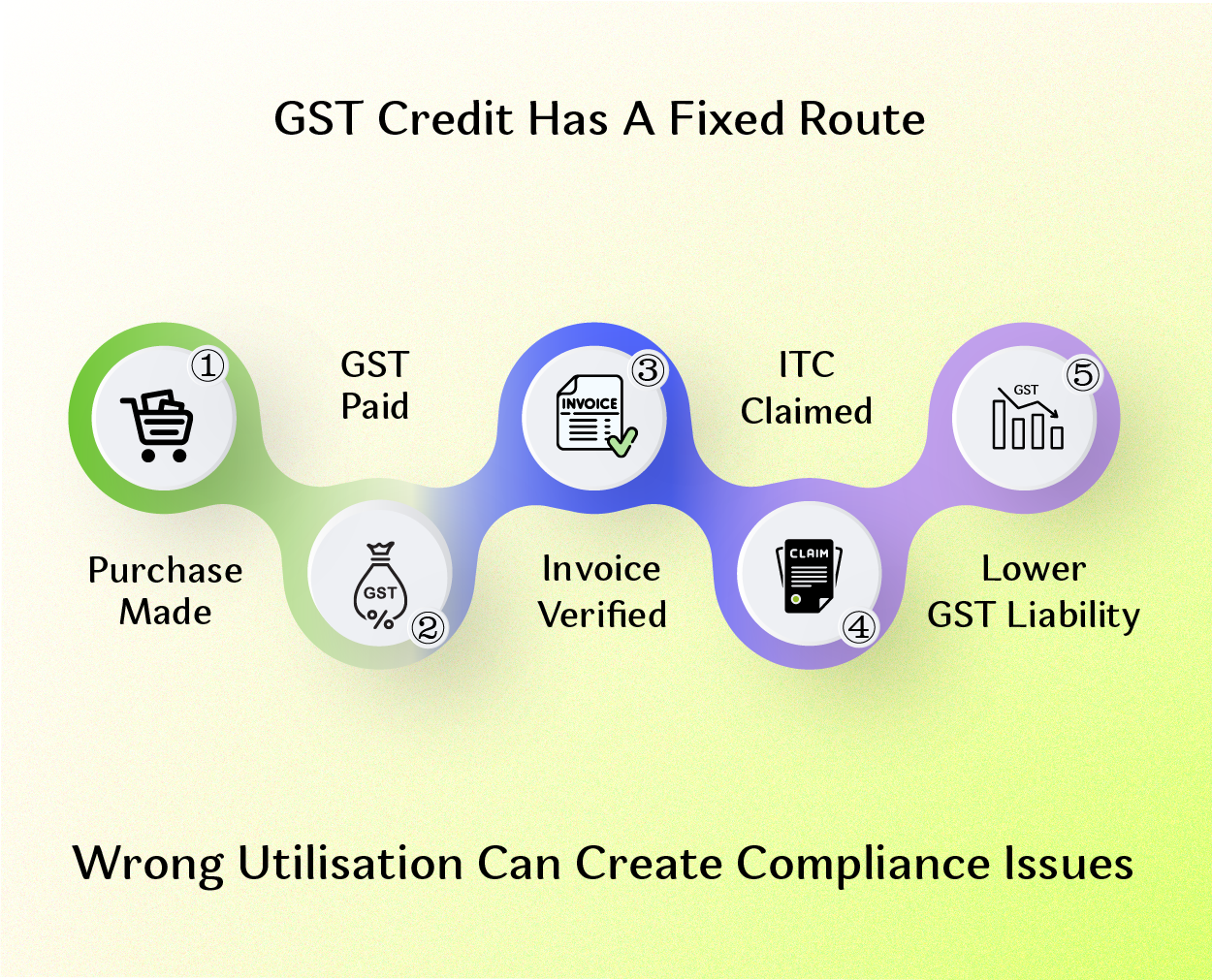

One wrong ITC claim can eventually become a future GST notice. Many businesses claim Input Tax Credit without fully understanding the eligibility rules, blocked credits, or reversal conditions, only to face interest, penalties, or denied credits later. When claimed correctly, ITC is one of the biggest financial advantages under GST. This improves cash flow and reduces double taxation. Understanding eligible and ineligible ITC, required documents, and reversal provisions is essential for accurate and compliant GST filing.

If you want to learn GST filing step by step and apply these concepts practically, explore the GST Filing with TallyPrime course.

Introduction

Input Tax Credit is the most important part of GST. It allows the registered business to claim credit for the GST paid on purchases which are used for business purposes. This in turn helps in reducing the tax liability as the tax is paid only on the value added at each point in the supply chain.

ITC Calculation Example: Manufacturer Buying Raw Materials

For example: Let us assume that a manufacturer purchases raw materials of ₹2,00,000 at 18% GST which is ₹36,000. Now, when the manufacturer makes the sale of the finished product for ₹3,00,000 at 18% GST it would sum up to ₹54,000. With the introduction of ITC, the Net tax payable by the manufacturer is ₹18,000 (54,000 – 36,000). Here, at the initial stage after making a purchase the manufacturer would take the claim of ₹36,000 as credit.

| Item | Amount |

|---|---|

| Purchases (Raw Materials) | ₹2,00,000 + ₹36,000 (18% GST) = ₹2,36,000 |

| Sales (Finished Product) | ₹3,00,000 + ₹54,000 (18% GST) = ₹3,54,000 |

| GST on Sales (Output Tax) | ₹54,000 |

| GST on Purchases (Input Tax Credit) | ₹36,000 |

| Net Tax Payable | ₹54,000 − ₹36,000 = ₹18,000 |

Benefits of ITC

1. Elimination of Cascading Tax Effect

ITC prevents the double taxation scenario. The tax is only collected on the value which is added at each stage.

2. Reduced Tax Liability

Businesses are required to only pay the net GST. That is by reducing the purchases from the sales.

3. Improved Cash Flow and Working Capital

With ITC being introduced, the burden on the businesses to pay the tax has now been reduced. This encourages liquidity, which is important for Small and Medium Enterprises.

4. Lowered Product Prices

The cost of production decreases as the tax burden on purchases is reduced. This in turn makes the goods and services more affordable for the end user.

5. Encourages Documentation and Compliance

To claim the ITC, the supplier must first file their returns which ensures the taxes are paid. Hence it encourages the business to maintain a transparent, documented, and compliant supply chain.

Eligible Input Tax Credit

ITC can be claimed when these below mentioned conditions are met by the supplier:

- Registered Person: The business must be registered and should have a GSTIN allotted to claim the ITC.

- Used for Business Purposes: Goods or services must mandatorily be used for business.

- Possession of Valid Tax Invoice: The supplier must issue a proper Tax Invoice (GST invoice).

- GST Paid by Supplier: The supplier must have filed the GSTR1 which ensures the tax is paid on time.

- Goods/Services Received: ITC can only be claimed once the goods or services are received.

- Return Filing: The required return such as GSTR-3B is to be filed without fail.

- Payment Timeline: The timeline of 180 days starting from the invoice date is being allotted to the buyer. This means that the payment is to be made to the supplier within the said timeline.

Examples of Eligible ITC

- Raw materials

- Packing materials

- Business rent

- Professional fees (CA, legal services)

- Machinery used for business

- Office supplies

Ineligible Input Tax Credit (Blocked Credits)

Under section 17(5) of the CGST Act, it is specified that the GST paid on specified goods or services cannot be claimed as a deduction against its tax liability. This is called Ineligible ITC or Blocked Credits.

Common Ineligible ITC Items

- Motor Vehicles: Except when used for transportation, training, or resale.

- Personal Expenses: Any goods or services used for personal consumption.

- Food & Beverages, Outdoor Catering: Unless mandatory under law (e.g., factory canteen).

- Club Memberships & Gym Fees: Because it is considered as personal consumption or employee welfare expenses.

- Travel Benefits to Employees: Vacation or leave travel benefits.

- Works Contract Services: For construction of immovable property (except plant & machinery).

- Goods Lost, Stolen, Destroyed, or Given as Free Samples: Because they are not used to make taxable supplies.

Forms and Documents Required for Claiming ITC Under GST

- Tax Invoice: A valid tax invoice issued by the supplier.

- Import bill of entry: To determine the amount of GST paid on imported goods.

- Delivery challans or Receipt Notes: Which plays as evidence for the goods being delivered.

- Credit Note: Issued by the supplier for adjustments related to return of goods.

- Debit Note: Issued by the supplier for adjustments such as price escalation.

- Form GSTR-3B monthly ITC claim.

- Form GST ITC-01 to claim ITC on stock in special cases (new registration, regular composition scheme, etc.)

- Invoice issued by Input Service Distributor (ISD) (Where applicable).

Order for Adjusting the ITC Against the Electronic Ledger

Input Tax Credit (ITC) available in the Electronic Credit Ledger must be used in a specific order when paying GST liability. The GST law sets clear rules for how this credit can be adjusted.

- IGST credit is used first to pay IGST liability. Any remaining amount can then be used to pay CGST or SGST/UTGST.

- CGST credit is used first to pay CGST liability. If any credit remains, it can be used to pay IGST, but not SGST/UTGST.

- SGST/UTGST credit is used first to pay SGST/UTGST liability. If any credit remains, it can be used to pay IGST, but not CGST.

- Cross-utilisation between CGST and SGST/UTGST is not allowed.

Input Tax Credit Reversal Under GST

Reversal of Input Tax Credit (ITC) means returning the tax credit which was claimed earlier by the business. ITC must be reversed in certain scenarios to ensure that the credit is claimed only for valid business-related expenses.

Common Scenarios for Reversal of ITC

- When the recipient fails to make the payment to the supplier within the 180 days of the invoice date.

- If the GST registration is cancelled or the scheme is changed to composition scheme.

- If the supplier fails to pay the collected GST by 30th of September of the previous financial year. Then the recipient will have to reverse the ITC by 30th of November.

- The reversal of ITC must be done if it is availed on blocked credits that are not allowed in Section 17(5) (e.g. motor vehicles used personally).

- If depreciation is claimed on the GST of capital goods under the Income Tax Act then the ITC on such tax should be reversed.

Wrapping Up

Input Tax Credit (ITC) is one of the most valuable features of the GST system. It ensures that tax is charged only on the value added at each stage. This helps businesses to avoid the cascading effect of taxes and reduce their overall tax burden.

However, claiming ITC requires proper documentation, timely payments to suppliers, and regular GST return filing. It is also needed that the businesses must clearly understand eligible and ineligible ITC and the scenarios where ITC reversal needs to be reversed.

When understood and managed correctly, ITC not only reduces tax liability but also improves the cash flow and strengthens GST compliance.

Frequently Asked Questions

Question 1: What is Input Tax Credit (ITC) under GST?

Answer: Input Tax Credit (ITC) allows registered businesses to claim credit for the GST paid on purchases when it is used for business purposes. This helps in avoiding double taxation and reduces the overall GST liability.

Question 2: Who is eligible to claim ITC under GST?

Answer: A registered taxpayer can claim ITC if the goods or services are purchased and either used for business purposes or further sold to end consumers.

Question 3: What are the conditions for claiming Input Tax Credit under GST?

Answer: To claim ITC under GST, businesses must:

- Have a valid GST invoice (Tax Invoice).

- Receive the goods or services.

- Ensure the supplier has paid GST.

- File GSTR-3B returns.

- Make payment to the supplier within 180 days.

Question 4: What is blocked credit or ineligible ITC under GST?

Answer: Blocked credit refers to goods or services on which ITC cannot be claimed under Section 17(5) of the CGST Act. Examples: Personal expenses, club memberships, food and beverages, and certain motor vehicles.

Question 5: When is ITC reversal required under GST?

Answer: ITC reversal is required in situations such as non-payment to suppliers within 180 days, claiming ITC on blocked credits, cancellation of GST registration, or when depreciation is claimed on GST paid for capital goods.

Question 6: Can ITC be claimed on capital goods under GST?

Answer: Yes, ITC can be claimed on capital goods used for business purposes, if depreciation is not claimed on the GST amount under the Income Tax Act.

Question 7. What documents are required to claim ITC under GST?

Answer: Businesses need documents such as a valid tax invoice, bill of entry, debit note, credit note, delivery challan, and GST return filings like GSTR-3B to claim ITC under GST.

Nita R

Nita is a content writer specialising in Accounting, Finance, GST, and Taxation. She creates easy-to-understand, research-driven content that simplifies complex financial and tax concepts for learners, professionals, and businesses. Her expertise lies in translating technical accounting and GST topics into practical insights, helping readers stay informed about tax compliance, financial processes, and industry best practices. Through her content, she aims to make accounting and taxation accessible, accurate, and relevant for today's evolving business environment.