Composition Scheme under GST

30-Second Summary

The Composition Scheme under the GST is a simplified tax option for small businesses in India such as small traders, manufacturers, restaurants, and certain service providers. Businesses with turnover below ₹1.5 crore in the previous financial year, are eligible for this scheme. The taxpayer must file the returns on a quarterly basis and pay GST at a reduced fixed rate on total sales.

This blog would help you to make an informed decision by outlining how the scheme works, who can opt for it, and its key benefits and drawbacks.

What Is the Composition Scheme Under GST?

The Composition Scheme under GST is a tax scheme designed for small businesses in India. Under this scheme, the eligible taxpayers are required to pay GST at a fixed and lower rate on the overall sales done. The tax compliance is much easier as the businesses must file the returns on a quarterly basis instead of monthly.

The limitations of this scheme are that the businesses are not allowed to claim the Input Tax Credit (ITC) and to collect GST from customers. It is best suited for small traders, manufacturers, and restaurants whose turnover has not exceeded ₹1.5 crore in the preceding financial year.

Eligibility Criteria

- Turnover Limit: A business must register under composition scheme if their AATO (Annual Aggregate Turn-Over) is below ₹1.5 crore in the previous financial year.

- Special Category States: For the listed 11 special category states, the turnover threshold is reduced to ₹75 lakh.

- Service Providers: GST has a special Composition Scheme designed for service providers as well. The businesses whose turnover in the last financial year was up to ₹50 lakh can opt for this scheme. This in turn makes the tax filing easier, even if they offer both services and a small supply of goods.

- All PAN-Based Units: If a taxpayer uses the same PAN for several business branches or segments. The scheme must be opted collectively by all companies registered under the same PAN.

Understanding the eligibility criteria is only the first step. Learn how the Composition Scheme is applied in real business transactions with our GST Simulation Course.

Types of Business under the composition scheme

- Manufacturers of Goods:

- Small manufacturers of the goods which are produced within the state.

- Manufacturers of goods like ice cream, pan masala, tobacco are not eligible.

- Traders (Retailers & Wholesalers):

- The Shopkeepers, traders, and small retail business owners whose business is carried on within the state.

- Restaurants (non-alcoholic):

- Restaurants and food service units that do not serve alcoholic beverages.

- Service Providers (Limited Eligibility):

- Dated from 2019, service providers with a turnover up to ₹50 lakh can opt for a special composition scheme.

- This focuses on small service sector units like repair shops, tailors, and salons.

- Brick Manufacturers:

- A separate composition rate is available for manufacturers of bricks, roofing tiles, and fly ash bricks.

| Business Category | Turnover Limit | Composition Tax Rate |

|---|---|---|

| Manufacturers | Up to ₹1.5 crore (₹75 lakh for North-Eastern states and Himachal Pradesh) | 1% of turnover (0.5% CGST + 0.5% SGST) |

| Traders (Goods) | Up to ₹1.5 crore (₹75 lakh for special category states) | 1% of turnover (0.5% CGST + 0.5% SGST) |

| Restaurants (Not Serving Alcohol) | Up to ₹1.5 crore | 5% of turnover (2.5% CGST + 2.5% SGST) |

| Service Providers (Other than Restaurants) | Up to ₹50 lakh | 6% of turnover (3% CGST + 3% SGST) |

| Brick Manufacturers (Specific Category) | Up to ₹20 lakh (₹10 lakh for special category states) | 6% without ITC for manufacturers of building bricks, fossil meal bricks, and earthen/roofing tiles. |

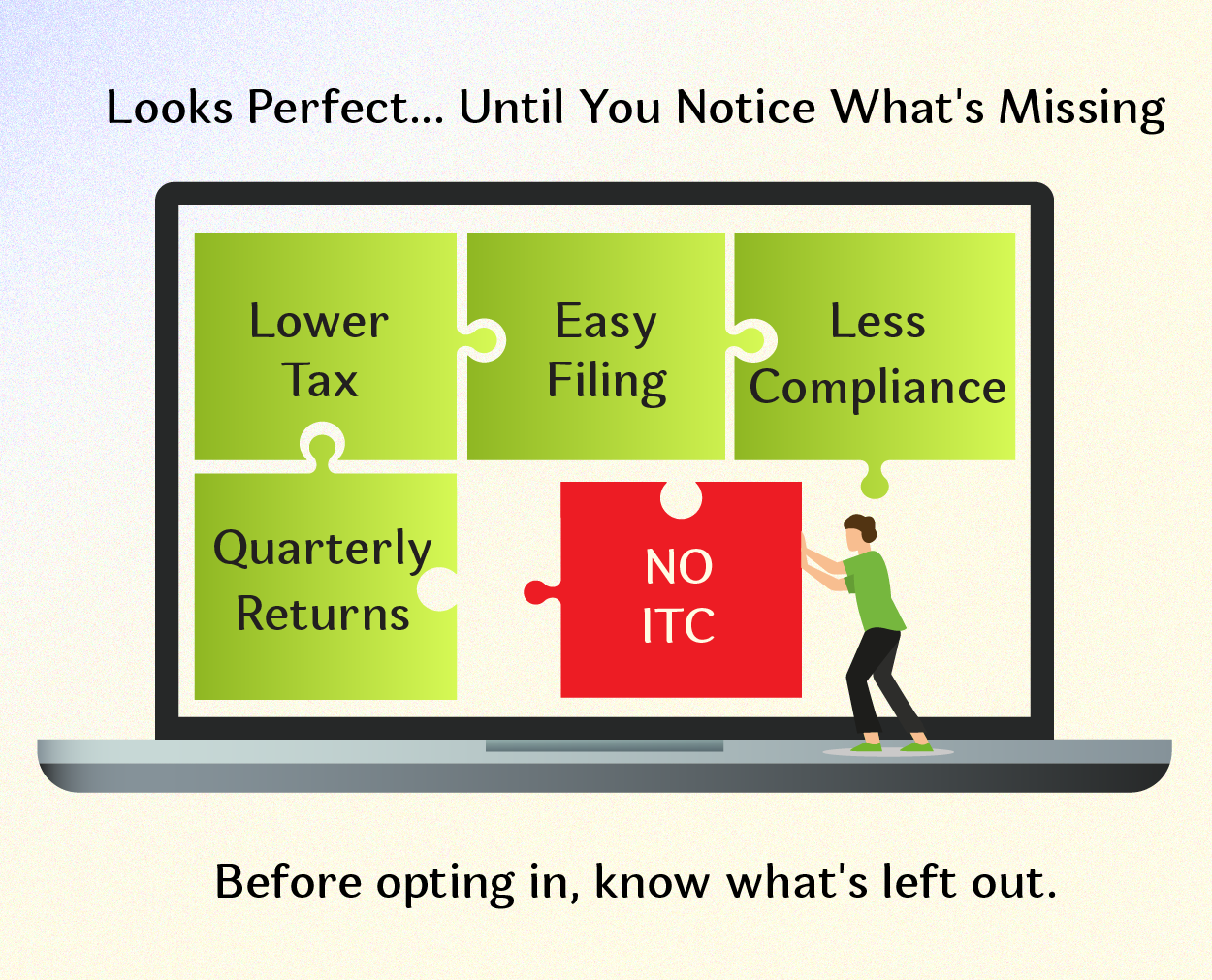

Advantages of the Composition scheme under GST

- Lower Tax Rates: Under the Composition Scheme, the eligible businesses can pay GST on their total sales at lower fixed rates. Compared to the standard GST rates, these rates are lower. It lessens the overall tax burden on small firms.

- Simplified Compliance: Unlike the regular dealers, the composite dealers are required to file fewer returns and maintain simpler records. This makes it easier for small taxpayers to manage GST obligations.

- Less Administrative Burden: The businesses can skip the hassle of maintaining complicated invoices and records. This in turn helps them to save time and focus more on running their business.

- Better Cash Flow Management: As the taxes are paid at a fixed rate on turnover, the businesses can estimate their tax liability. This would enable them to plan their finances more effectively.

- Suitable for Small Businesses: The Composition Scheme simplifies GST compliance for small businesses. This allows them to concentrate more on their core operations and productivity.

- Reduced Cost of Compliance: The filing process and record-keeping requirements are much simpler. This means that the businesses can save on accounting and professional fees spent on the accountants and CAs.

- Easy Tax Calculation: The calculation part of tax is much easier as it is calculated on the overall sales done in a quarter. This makes it easy for the business to determine the amount of tax to be paid.

Disadvantages of the Composition Scheme under GST

- No Input Tax Credit (ITC) Allowed: Composition dealers cannot claim credit (ITC) for the GST paid on purchases of raw materials, goods, or services. The tax paid by them becomes an additional cost which increases the overall cost of operations.

- Restricted Interstate Sales and exports: Businesses under this scheme are not allowed to make interstate sales and export of goods. They are permitted to sell goods only within their state of registration. This plays a key role in limiting the market expansion.

- Cannot Issue Tax Invoices: A composition dealer must issue “Bill of Supply” instead of “Tax Invoice”. Therefore, they cannot charge and collect GST from their customers. Which means the tax must be paid by the dealer himself.

- B2B Disadvantage: The regular dealers often prefer not to purchase from the composite dealers as they cannot claim credit (ITC). This makes them less competitive in the Business-to-Business (B2B) market.

- No E-commerce Sales: Suppliers who sell goods through e-commerce operators (e.g., Amazon, Flipkart) are not eligible to opt for the composition scheme.

- Exclusion of Non- Taxable Goods: The supply of non-taxable goods such as alcohol for human consumption are excluded from this scheme.

- Applicability of Reverse Charge Mechanism: The composite dealers must pay GST under the Reverse Charge Mechanism (RCM) on specified purchases on behalf of the supplier.

Returns and Reports for Composition Scheme

Taxpayers registered under the composition scheme have simplified return filing requirements compared to regular GST taxpayers.

- GSTR-4 (Annual Return): Composition taxpayers must file GSTR-4 annually, which contains business’s total turnover, inward supplies, and tax paid during the financial year. The due date for filing the GSTR-4 is on 30th April of the following financial year. One must ensure filing returns on time is important to avoid penalties and interest charges under GST.

- CMP-08 (Quarterly Statement): Composition taxpayers must file CMP-08 every quarter which includes the summary of the overall sales, tax payable, and tax payment details. The due dates for filing the CMP-08 are as follows:

- April – June: 18 July

- July – September: 18 October

- October – December: 18 January

- January – March: 18 April

Related Read: E-Invoicing Under GST: Rules, Eligibility & Process Explained

Key differences between a regular and a composition dealer

| Basis | Regular Dealer | Composition Dealer |

|---|---|---|

| Tax Rate | Pays GST at normal rates applicable to goods or services. | Pays tax at a fixed lower rate on total turnover. |

| Input Tax Credit (ITC) | Can claim Input Tax Credit on purchases. | Cannot claim Input Tax Credit. |

| Collection of GST | Can collect GST from customers and show it separately on invoices. | Cannot collect GST separately from customers. |

| Type of Invoice | Issues a Tax Invoice. | Issues a Bill of Supply instead of a tax invoice. |

| Compliance Requirements | Requires detailed records and multiple return filings. | Compliance is simpler with fewer returns and less documentation. |

| Inter-State Sales | Can sell goods or services across states. | Not allowed to make inter-state outward supplies. |

| Eligibility | Available to all eligible GST-registered businesses. | Available only to small businesses within specified turnover limits. |

| Suitability | Suitable for medium and large businesses or B2B transactions. | Suitable for small businesses dealing mainly with end consumers. |

Composition Scheme at a Glance

The Composition Scheme under the Goods and Services Tax is the best tax option for small businesses in India. This scheme allows eligible businesses to pay GST at a fixed and lower rate on their overall sales. The filing is done once in every quarter.

The scheme is helpful for small traders, manufacturers, and restaurants-based businesses. It reduces paperwork and makes tax filing easier. However, the scheme has its own limitations, where no Input Tax Credit can be claimed, and interstate sales are not permitted.

All things considered, the Composition Scheme is a reasonable choice for small firms which are seeking less complicated taxation and easier GST compliance.

Frequently Asked Questions about Composition Scheme

Question 1: What is the Composition Scheme under GST?

Answer: The Composition Scheme under GST is a simplified tax scheme exclusively built for small businesses where the taxpayers pay GST at a fixed lower rate on overall sales and file returns quarterly.

Question 2: Who is eligible for the Composition Scheme under GST?

Answer: Small businesses with turnover up to ₹1.5 crore in the previous financial year can opt for the Composition Scheme under GST. For certain special category states, the turnover limit is ₹75 lakh.

Question 3: Can service providers opt for the Composition Scheme under GST?

Answer: Yes, service providers with turnover up to ₹50 lakh can opt for a special Composition Scheme and pay GST at a concessional rate, subject to prescribed conditions.

Question 4: What are the benefits of the Composition Scheme under GST?

Answer: The Composition Scheme offers lower GST rates, simplified compliance, quarterly return filing, reduced paperwork, and easier tax calculation for small businesses.

Question 5: Can composition dealers claim Input Tax Credit (ITC)?

Answer: No, taxpayers registered under the Composition Scheme cannot claim Input Tax Credit (ITC) on purchases made for business purposes.

Question 6: What is the difference between a regular dealer and a composition dealer under GST?

Answer:

| Regular Dealer | Composition Dealer |

|---|---|

| Can claim Input Tax Credit (ITC) | Cannot claim Input Tax Credit (ITC) |

| Can make inter-state sales | Restricted from making inter-state sales |

| Can collect GST from customers | Cannot collect GST from customers |

| Issues a Tax Invoice | Issues a Bill of Supply |

Question 7: Which returns are filed under the Composition Scheme?

Answer: Composition taxpayers are required to file CMP-08 quarterly and GSTR-4 annually under the GST Composition Scheme.

Nita R

Nita is a content writer specialising in Accounting, Finance, GST, and Taxation. She creates easy-to-understand, research-driven content that simplifies complex financial and tax concepts for learners, professionals, and businesses. Her expertise lies in translating technical accounting and GST topics into practical insights, helping readers stay informed about tax compliance, financial processes, and industry best practices. Through her content, she aims to make accounting and taxation accessible, accurate, and relevant for today's evolving business environment.